Every generation has opportunities that can shape the financial future of the next. Sometimes those opportunities come from changes in the tax code. Other times they come in the form of new savings and investment vehicles designed to encourage long-term wealth creation.Trump Accounts are one of those opportunities.

Since they were introduced, they've generated a great deal of discussion and just as many questions. Parents want to know whether they should open one for their children. Grandparents are wondering if this is a worthwhile gift. Business owners are asking whether employer contributions make sense. And many families are trying to understand how these accounts fit alongside 529 plans, custodial accounts, and other long-term savings strategies.

Like any new financial program, understanding how it works is the first step toward deciding whether it belongs in your family's financial plan.

Let's take a closer look.

What Is a Trump Account?

A Trump Account is a long-term investment account created to help children begin building wealth early in life. Eligible children may receive a one-time $1,000 contribution from the federal government, and additional contributions can be made by parents, grandparents, employers, and others, subject to annual contribution limits established by law.

One feature that makes these accounts unique is that the child does not need earned income to participate. Unlike a Roth IRA or Traditional IRA, eligibility isn't tied to having a job or reporting wages.The account is designed to begin investing early, giving children something that no investment strategy can replace…time. When money has decades to grow, even modest contributions can benefit from the power of long-term compounding.

Why Starting Early Matters

Many people assume building wealth requires large sums of money.

In reality, time is often the more valuable asset.

Consider two young investors. One begins investing during childhood and continues making consistent contributions over many years. The other waits until adulthood before getting started. Even if the second investor contributes more each year, they have fewer years for their investments to grow.

That's one of the principles behind Trump Accounts.

The earlier investing begins, the longer earnings have the opportunity to generate additional earnings. Over several decades, that compounding effect can become significant. No one can predict future investment returns, but history has consistently shown that disciplined investing over long periods has rewarded patient investors.

Who Can Open a Trump Account?

Trump Accounts are available only for eligible children who meet the requirements established by the legislation. Children must have a valid Social Security number, and the account must be opened before the applicable age deadline.

An authorized adult manages the account until the child reaches adulthood. In most cases, that responsibility falls to a parent or legal guardian, although other family members may qualify under certain circumstances. While opening the account itself is relatively straightforward, families should pay close attention to eligibility requirements and important deadlines. Missing them could mean losing the opportunity to establish the account.

Understanding Contributions

The government's initial contribution has received most of the public attention, but it represents only one part of the account's funding. Families may continue making contributions each year, up to the annual limit established by law. Parents, grandparents, relatives, and friends can all play a role, provided total contributions remain within the allowable amount. Some employers may also choose to contribute to an employee's child's account through qualified benefit programs.

This creates an interesting opportunity for families who want multiple generations participating in a child's financial future. Because the annual contribution limit applies to the child (not to each individual contributor) parents and grandparents should coordinate their gifts throughout the year. Be sure to keep communication open, as it's possible for well-intentioned family members to exceed the annual limit.Keeping accurate records of who contributed and how much is equally important. Different contribution sources may receive different tax treatment over time, making good documentation a valuable habit from the beginning.

How the Money Is Invested

Unlike many investment accounts, Trump Accounts don't allow unlimited investment choices during a child's early years.Instead, investments are generally limited to broadly diversified, low-cost funds that track the U.S. stock market. For some investors, those restrictions may seem limiting.

From a long-term planning perspective, however, they encourage a disciplined approach built around diversification, low expenses, and patience rather than speculation. Children don't need concentrated portfolios or complex investment strategies. They need time. Broad market exposure combined with decades of compounding has historically been a powerful combination for long-term investors. Once the beneficiary reaches adulthood, the investment options become much more flexible under the rules governing the account at that stage.

What Happens When the Child Turns 18?

One of the most important features of a Trump Account is what happens when childhood ends. As the beneficiary reaches adulthood, the account transitions under traditional retirement account rules. That transition opens the door to additional planning opportunities, including broader investment choices and, depending on the individual's tax situation, the possibility of converting assets to a Roth IRA.

This isn't a decision to make automatically. Income, tax brackets, future earnings, and IRS guidance all play an important role in determining whether a Roth conversion makes sense. For some young adults, converting early could provide decades of tax-free growth. For others, waiting may be the more appropriate choice.

Every situation deserves thoughtful analysis rather than a one-size-fits-all approach.

Trump Accounts and 529 Plans: Understanding the Difference

One of the first comparisons many families make is between a Trump Account and a 529 college savings plan. While both encourage long-term saving, they were designed with different goals in mind. A 529 plan exists primarily to help families save for qualified education expenses and may provide valuable tax advantages depending on where you live. A Trump Account focuses on retirement savings and long-term investing beginning early in life.

For many families, these aren't competing strategies. They simply solve different problems. Parents who want to prepare for future education expenses may still find tremendous value in a 529 plan. Families who also want to help a child establish retirement savings decades before entering the workforce may see value in adding a Trump Account as part of a broader financial plan.

Understanding the purpose of each account makes it easier to determine how they can work together.

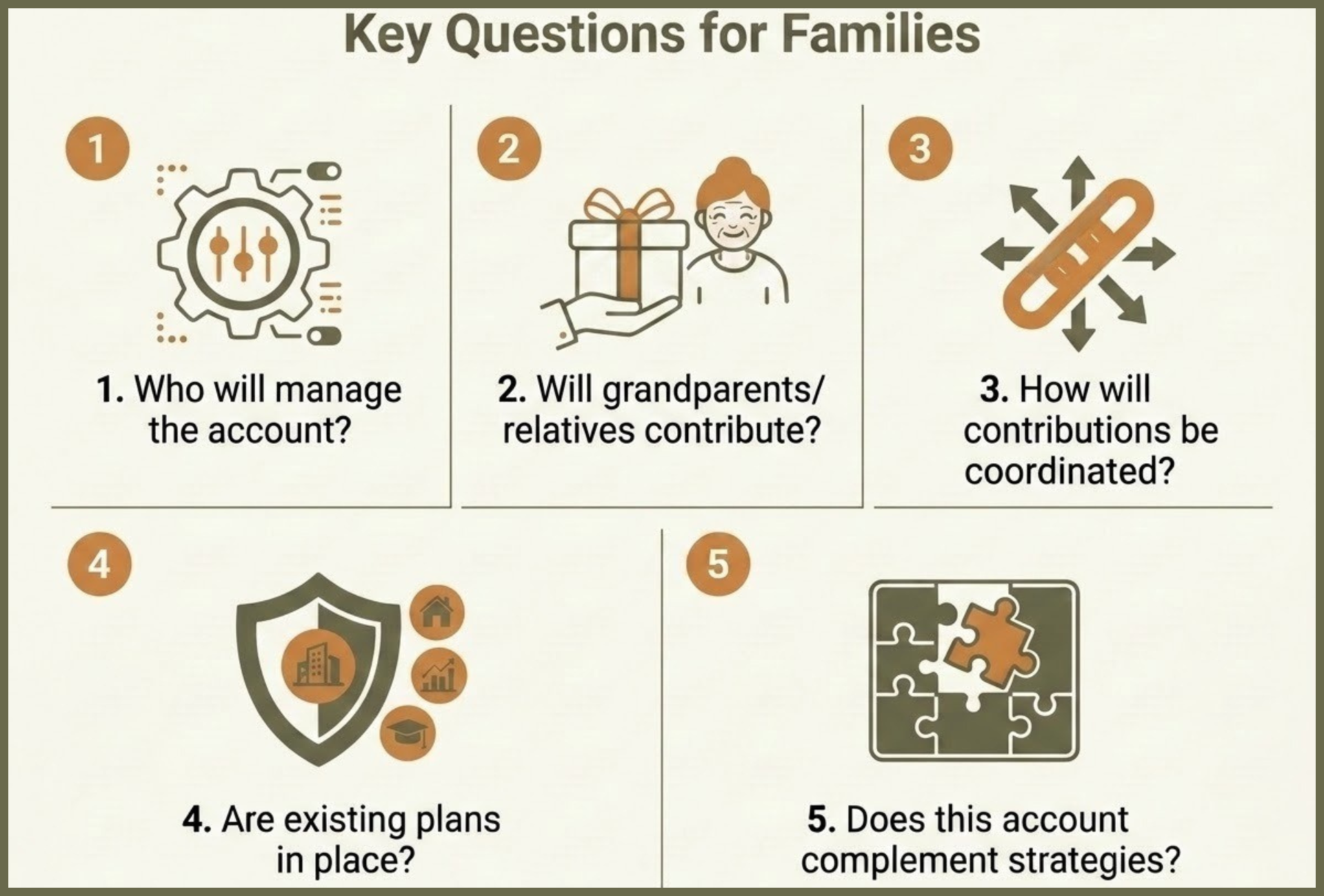

Questions Worth Asking Before Opening an Account

Whenever a new financial opportunity becomes available, enthusiasm often arrives before understanding. Before opening a Trump Account, families should take time to consider a few practical questions.

The answers will look different from one family to another.That's perfectly normal.

Financial planning has never been about finding one solution that works for everyone. It's about understanding the tools available and using the ones that align with your family's goals.

A Long-Term Opportunity

Trump Accounts are still new, and additional guidance will continue to shape how families use them in the years ahead. Even so, the principle behind them is familiar.

Start early. Invest consistently. Allow time to do much of the work.

Parents and grandparents have always looked for meaningful ways to invest in the next generation. For some, that means helping with college. For others, it's assisting with a first home, supporting a family business, or creating a lasting legacy through thoughtful estate planning. A Trump Account adds another option to that list.

Whether it's the right option depends on your family's priorities, financial resources, and long-term objectives.Programs will change. Tax laws will evolve. New opportunities will continue to emerge.The principles of successful financial planning rarely do.

Clear goals, disciplined investing, thoughtful decision-making, and a long-term perspective have helped families build wealth for generations. Those same principles will continue to matter long after today's headlines have faded.

Ralph Adamo is registered with, and securities are offered through Kovack Securities, Inc., Member FINRA/SIPC, 6451 N. Federal Highway, Suite 1201, Ft. Lauderdale, FL 33308. Tel: 954-782-4771.

Investment Advisory services are offered through Kovack Advisors, Inc. Integrity Wealth Management is not affiliated with Kovack Securities, Inc. or Kovack Advisors, Inc.

The information contained in this article is provided for educational and informational purposes only and should not be construed as investment, legal, or tax advice, or as a recommendation to buy or sell any security or implement any financial strategy. The views expressed are those of the author as of the date of publication and are subject to change.

Please consult your legal, tax, and financial professionals regarding your individual circumstances before making any financial decisions.